Professor Chien-Feng Huang discusses how Artificial Intelligence could provide innovative models and strategies to solve investment problems

Over the past decade, Professor Chien-Feng Huang has been working on several investment problems using Artificial Intelligence (AI). Big Data technology, data mining and machine learning play crucial roles in his research, where he hopes to discover niches and innovative solutions to bring about blue ocean strategies for investment.

One major line of research Professor Huang has been pursuing is to combine seemingly contradictory strategies to generate emerging solutions for investment. For example, the momentum investing strategy might advise buying a stock, yet the value investment strategy advises against it. So, which one is right?

Are further solutions created by combining these contradictory strategies to supersede the old ones? In other situations, various useless strategies, when fine-tuned, often become critical components of a powerful investment toolset. For such questions, Professor Huang’s research showed that AI-based methodologies are promising in assisting with solving such problems.

Genetic algorithms to construct investment models

It turns out that problems with multiple conflicting strategies can be transformed into a class of combinatorial problems frequently studied in operation research and optimization. To shed light on such combinatorial optimization problems, as an illustration, Professor Huang and his team employed Genetic algorithms (GA) (1) to construct novel intelligent dynamic investment models by properly combining value investment and momentum investment strategies.

In the model, they selected five momentum indicators: Trading volumes for individual stocks, trading values for individual stocks, net buy/sell value of three institutional investors, net buy/sell volume of three institutional investors, and monthly return rates. Six value indicators were also selected, including price-earnings ratio (PE), return on assets (ROA), return on equity (ROE), dividend yield, and year-on-year revenue growth rate (YOY). Then, the GA is used to evolve models with optimal weights and factors for the momentum and value investment strategies.

Genetic algorithms are well-known as a class of adaptive algorithms which solve optimization problems. GA operate on an evolving population of artificial agents. Each agent comprises a genotype (often a binary string) encoding a solution to some problem and a phenotype (the solution itself). During evolution, new generations are created through selection, crossover and mutation to produce fitter agents (solutions) to solve a problem. The core of GA lies in the production of new genetic structures through evolution, which gradually provides innovative solutions for the problem at hand.

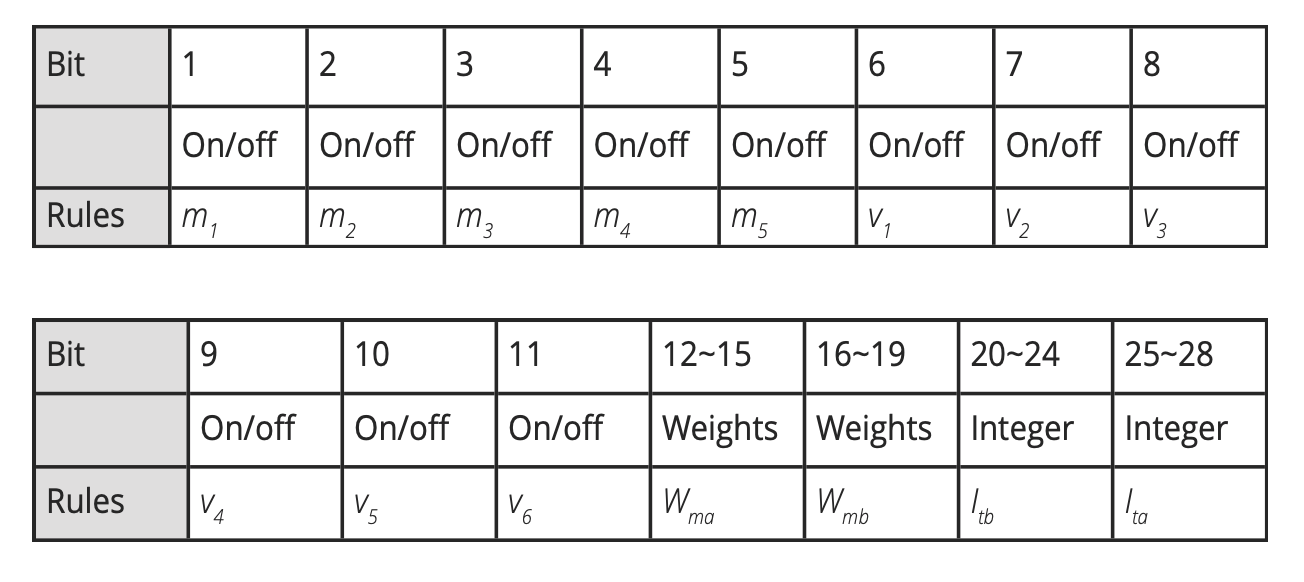

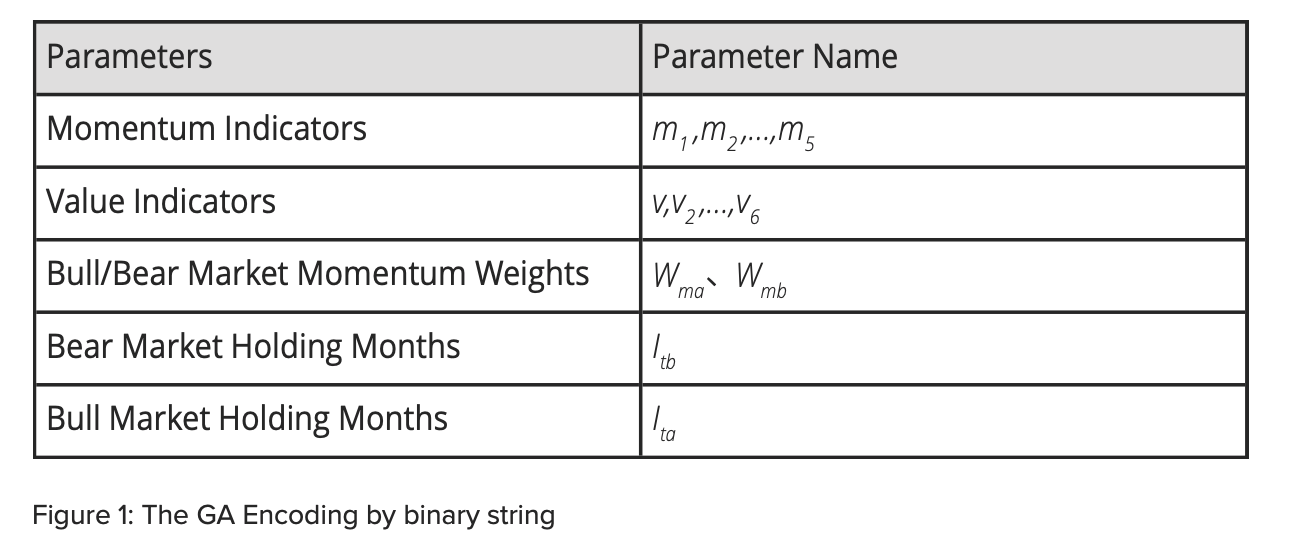

The parameters in the encoded strings are:

The parameters in the encoded strings are:

Utilizing binary encoding

As suggested by Huang (2) and as demonstrated by Huang and his lab members, to solve the combinatorial problems of momentum and value strategies, the optimization of indicators selection, value and momentum indicator, weights as well as holding durations can be achieved through the GA. For instance, they utilized binary encoding for the investment models. Each model consists of several binary-string blocks, with each block of 28 bits as displayed in the following table:

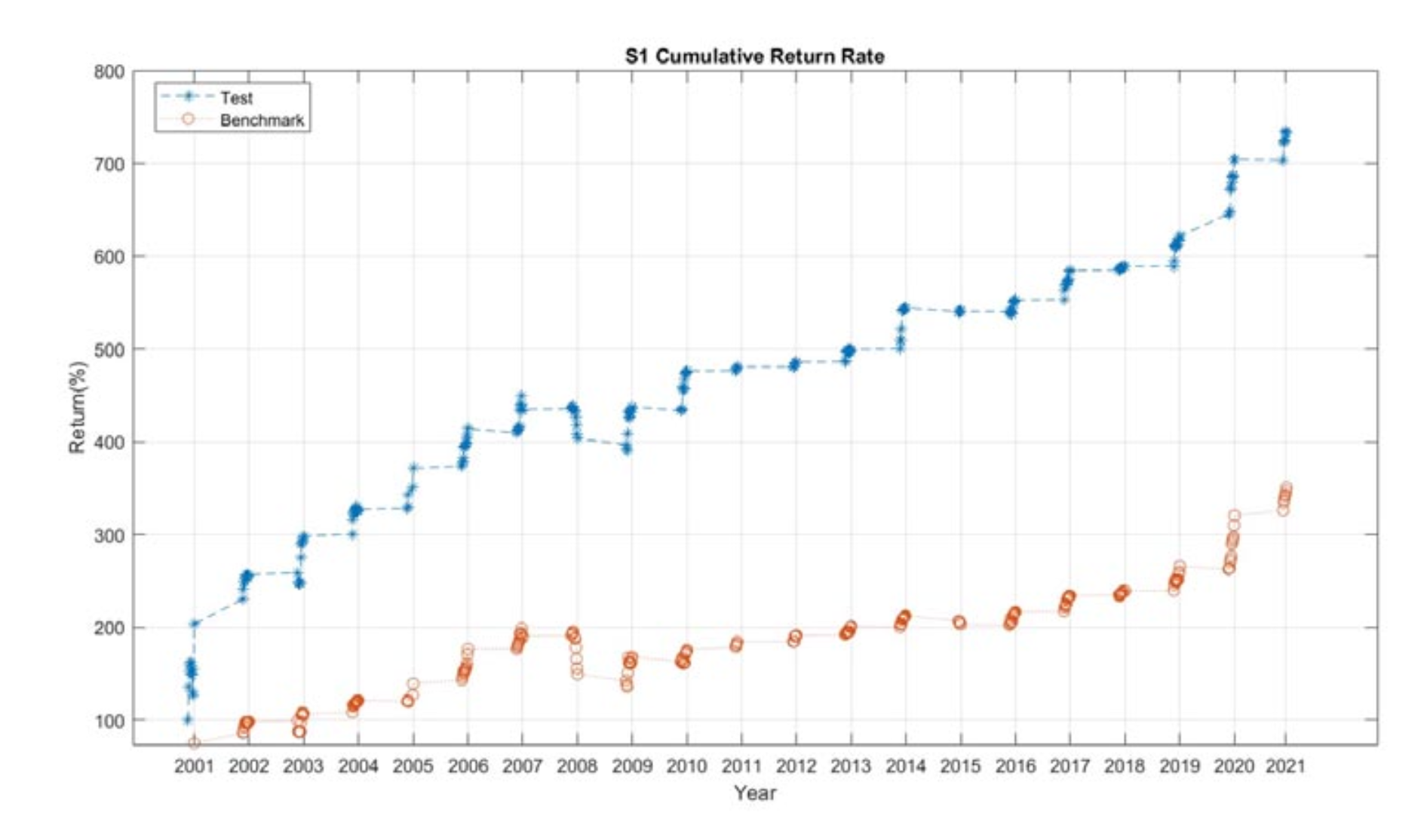

Some illustrative results are shown in the figure below, where the red curve is the investment performance of the benchmark (Taiwan Stock Exchange Capitalization Weighted Stock Index) and the blue curve is the proposed model. The performance discrepancy is getting more significant along the course of investment.

Conclusion

The research findings also indicate that the primary indicators affecting the model performance include the momentum indicators ‘monthly return rate,’ as well as value indicators such as ‘dividend yield’ and ‘price-earnings ratio.’ During bullish periods, the weight of the momentum indicators was notably higher than that of the value indicators. In contrast, during bearish periods, the effects of value indicators were more significant than the moment indicators.

This observation highlights the characteristics of investment in the stock market of Taiwan: during bullish and bearish periods, momentum strategies and value strategies are more useful, respectively. Thus, the results of this research can serve as a valuable reference for investors.

Acknowledgement

The content of this article is primarily adapted from the research work of Miss Ya-Yun Cheng, under the supervision of Professor Chien-Feng Huang.

References

- J. H. Holland, Adaptation in Natural and Artificial Systems, University of Michigan Press, Ann Arbor, Michigan, USA, 1975.

- C.-F. Huang, “High-frequency trading through artificial intelligence for financial innovation” 2023.

This work is licensed under Creative Commons Attribution-NonCommercial-NoDerivatives 4.0 International.